How to Calculate Your Monthly Loan Payment (EMI)

Knowing your monthly loan payment before you borrow is one of the smartest financial habits you can build. That fixed amount, often called the EMI or equated monthly installment, decides how a loan fits into your budget and how much interest you pay over the years. Once you understand how it is calculated, you can compare loans with confidence instead of guessing.

This guide explains what your monthly loan payment is made of, the three numbers that shape it, and how to work it out in seconds.

What Makes Up a Monthly Loan Payment

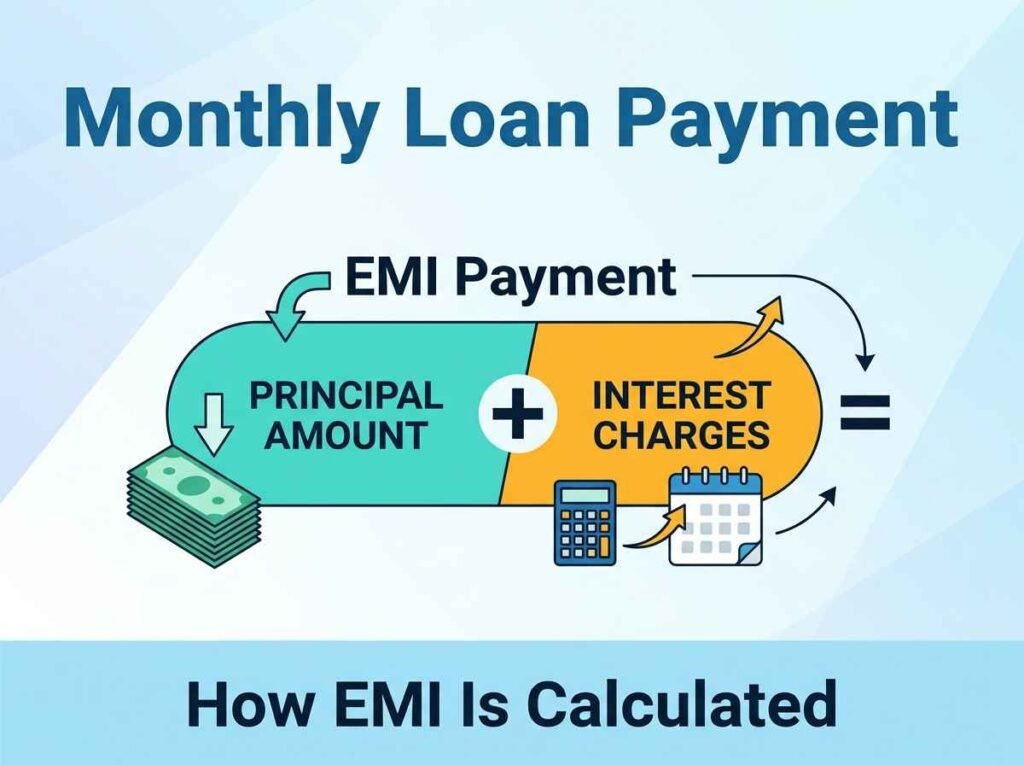

Every monthly loan payment covers two things: a slice of the amount you borrowed, called the principal, and the interest charged on what you still owe. Early in a loan, most of each payment goes toward interest. As the balance shrinks, more of each payment chips away at the principal. The payment amount stays the same, but the split shifts over time.

This is why two loans with the same monthly payment can cost very different amounts overall. The term and the rate quietly decide how much of your money goes to interest versus actually paying down the debt.

The Three Numbers That Decide Your Payment

Your monthly loan payment depends on just three inputs:

- Loan amount (principal) — the total you borrow. A bigger principal means a bigger payment.

- Interest rate — the annual rate the lender charges. Even a small difference adds up over a long term.

- Loan term — how long you take to repay. A longer term lowers the monthly payment but raises the total interest.

Change any one of these and your payment changes. That is the key insight: you can often make a loan affordable by adjusting the term, but you should always check what that does to the total interest before deciding.

The Formula Behind EMI

The monthly payment is calculated with a standard formula that spreads the loan and its interest evenly across every month of the term. In plain terms, it takes your principal, applies the monthly interest rate, and divides everything so that the same amount is paid each month until the balance reaches zero.

You do not need to do this by hand. The formula is fiddly and easy to get wrong, especially over long terms. Instead, enter your three numbers into a loan and EMI calculator and it does the math instantly, including the total interest and a full repayment schedule.

How to Calculate Your Payment Step by Step

Here is the simple process using a calculator:

- Enter the loan amount you plan to borrow.

- Enter the annual interest rate offered by the lender.

- Enter the term in years or months.

- Read off your monthly payment, total interest, and total amount repaid.

From there, try lowering the term to see how much interest you save, or raising it to see how much the monthly payment drops. This quick experimentation is the real benefit of using a calculator over a one-time formula.

Why Total Interest Matters as Much as the Payment

It is tempting to focus only on the monthly number, but the total interest is where loans get expensive. Stretching a loan over a longer term makes each payment smaller and easier, yet you may end up paying far more overall because interest keeps accruing for more years.

A good rule is to choose the shortest term you can comfortably afford. The loan and EMI calculator shows the principal-versus-interest split so you can see exactly how much a longer term really costs before you commit. Even a modest extra payment each month can shorten the loan and cut the total interest noticeably, so it is worth testing a few scenarios before you sign.

Frequently Asked Questions

What does EMI stand for?

EMI means equated monthly installment, the fixed amount you pay each month until a loan is fully repaid. It covers both interest and principal.

Does a longer loan term reduce my payment?

Yes, but it usually increases the total interest. A longer term lowers the monthly amount while adding more payments overall.

Is this the same calculation for a mortgage and a car loan?

Yes. The same EMI formula applies to mortgages, car loans, and personal loans that have a fixed rate and equal monthly payments.

How can I lower my monthly payment?

You can lower it by borrowing less, finding a lower interest rate, or choosing a longer term — though a longer term raises the total interest you pay.

Work Out Your Payment Now

You do not have to wonder what a loan will cost. Open the loan and EMI calculator, enter your numbers, and see your exact monthly payment and total interest in seconds. For the bigger picture on planning your money, read our guide to the free financial calculators everyone should use.